Last Updated on March 14, 2026 by Staff Writer

China’s upcoming 15th Five-Year Plan (2026–2030) marks a decisive shift in the global technology landscape. Rather than focusing primarily on economic growth, Beijing is doubling down on technological sovereignty and industrial independence, particularly in hardware sectors such as semiconductors, AI accelerators, robotics, and advanced manufacturing.

For global hardware vendors—and for industries that rely heavily on embedded computing, displays, and edge devices—this policy framework could reshape supply chains and competitive dynamics over the next decade.

Opinion from Investor — The US tends to be ad hoc reactionary when it comes to policy and law and incentives. Plus the current administration seems to discourage new technology (solar, EV). With the added stimulus of a war in Middle East changes in Asia must be expected. While the energy disruption will be a headache for China they will most likely double down on accelerating all forms of technology and energy. Now is their best opportunity given confusion in DC. Fossil/old tech basis will lose to Renewable/New Tech eventually. I’m afraid DC is too simplistic and optimistic without a firm foundational basis. I come from Oil and Gas industry myself.

From “World’s Factory” to Innovation Powerhouse

China’s economic strategy is evolving. The country is attempting to transition from low-cost manufacturing to high-value innovation-driven growth by 2030.

The 15th Five-Year Plan is the primary policy instrument for that transformation. It coordinates investment, subsidies, and regulation across multiple strategic sectors.

Key objectives include:

-

Achieving scientific and technological self-reliance

-

Upgrading traditional manufacturing into advanced digital industries

-

Reducing dependence on foreign technology suppliers

-

Strengthening domestic supply chains

These priorities are driven partly by geopolitical pressures, including export controls and technology restrictions imposed by the United States and its allies.

As a result, Beijing is shifting policy from “innovation discovery” to “innovation deployment”—meaning the emphasis is no longer just research breakthroughs but mass commercialization of domestic technology.

Massive Investment in Technology Infrastructure

The scale of China’s investment push is enormous.

Key figures already emerging from policy announcements include:

-

R&D spending target: more than 7% annual growth during the plan period

-

Total R&D spending: roughly $570 billion annually (2025 levels)

-

Basic research funding: nearly 280 billion yuan ($40+ billion) annually

-

Infrastructure investment: about 7 trillion yuan ($1 trillion) in AI computing and power grid infrastructure

These figures place China among the world’s largest technology investors, rivaling or surpassing many Western economies in public industrial policy.

The government is also expanding specialized investment funds. One semiconductor fund alone—known as the “Big Fund”—has injected tens of billions into domestic chip companies to accelerate development of critical technologies.

Hardware Independence Is the Strategic Goal

At the center of the 15th Five-Year Plan is a push for hardware sovereignty.

China’s leadership has identified several “core technologies” that must be domestically controlled:

Semiconductors

China is investing heavily in chip fabrication and equipment manufacturing. The country aims to dramatically expand advanced chip production capacity, with some projections targeting 500,000 monthly wafer starts at advanced nodes by 2030.

Domestic chipmakers such as SMIC and Hua Hong are expanding capabilities, while equipment firms like Naura and AMEC are developing alternatives to Western tools.

Artificial Intelligence Hardware

AI processors and accelerators are another priority area. Huawei, for example, is building large-scale AI computing clusters powered by domestic Ascend AI chips in an effort to compete with U.S. systems built around Nvidia GPUs.

Industrial Automation

Robotics and automated manufacturing are expected to expand rapidly as China addresses labor shortages and productivity goals.

Advanced Materials and Machine Tools

The plan also prioritizes high-end instruments, industrial software, and advanced materials to complete domestic supply chains.

Policy Tools: Subsidies, Standards, and Domestic Substitution

Beijing’s approach combines several mechanisms:

1. State Investment

Government funding supports both startups and large national champions.

2. Domestic Procurement Rules

In some sectors, regulators are pushing manufacturers to use domestic equipment whenever possible, encouraging substitution away from foreign suppliers.

3. National Standards

China is also working to shape global technology standards in emerging fields such as AI infrastructure, smart manufacturing, and data governance.

These policies collectively create an ecosystem designed to scale domestic technology quickly, even when it initially lags global competitors.

Implications for Global Hardware Vendors

The push for technological self-reliance has major implications for international companies.

Shrinking Market Access

Foreign vendors may face increasing pressure as Chinese firms are prioritized in government procurement and strategic industries.

New Competitors

Chinese companies are rapidly improving capabilities in:

-

industrial PCs

-

embedded computing

-

AI accelerators

-

robotics

-

display manufacturing

Fragmentation of Global Supply Chains

Technology supply chains could become increasingly regionalized, with separate ecosystems emerging in China, the United States, and Europe.

This shift is already visible in semiconductors, where export controls and industrial subsidies are driving a global race to localize production.

What It Means for Self-Service Hardware

For industries such as kiosks, digital signage, and unattended retail, China’s strategy could have several effects.

More Domestic Edge Computing Platforms

Chinese vendors are likely to expand production of mini-PCs, ARM edge processors, and AI modules designed for retail and public infrastructure.

Lower-Cost Hardware Ecosystems

Mass domestic production could drive down prices for components such as displays, touchscreens, and embedded processors.

Faster AI Integration

Edge AI hardware developed under the plan may accelerate adoption of:

-

computer vision

-

automated checkout

-

facial authentication

-

voice-enabled interfaces

In other words, the same industrial policy shaping semiconductors and robotics may also influence the next generation of self-service hardware platforms.

The Global Tech Competition Era

China’s 15th Five-Year Plan represents more than economic policy—it is part of a broader global technology competition.

Beijing’s strategy is clear: build a complete domestic ecosystem capable of designing, manufacturing, and deploying advanced technology without relying on foreign suppliers.

For the rest of the world, the implications are significant. The coming decade may see parallel technology ecosystems emerge across major geopolitical blocs.

Hardware industries—from semiconductors to kiosks—are likely to be at the center of that transformation.

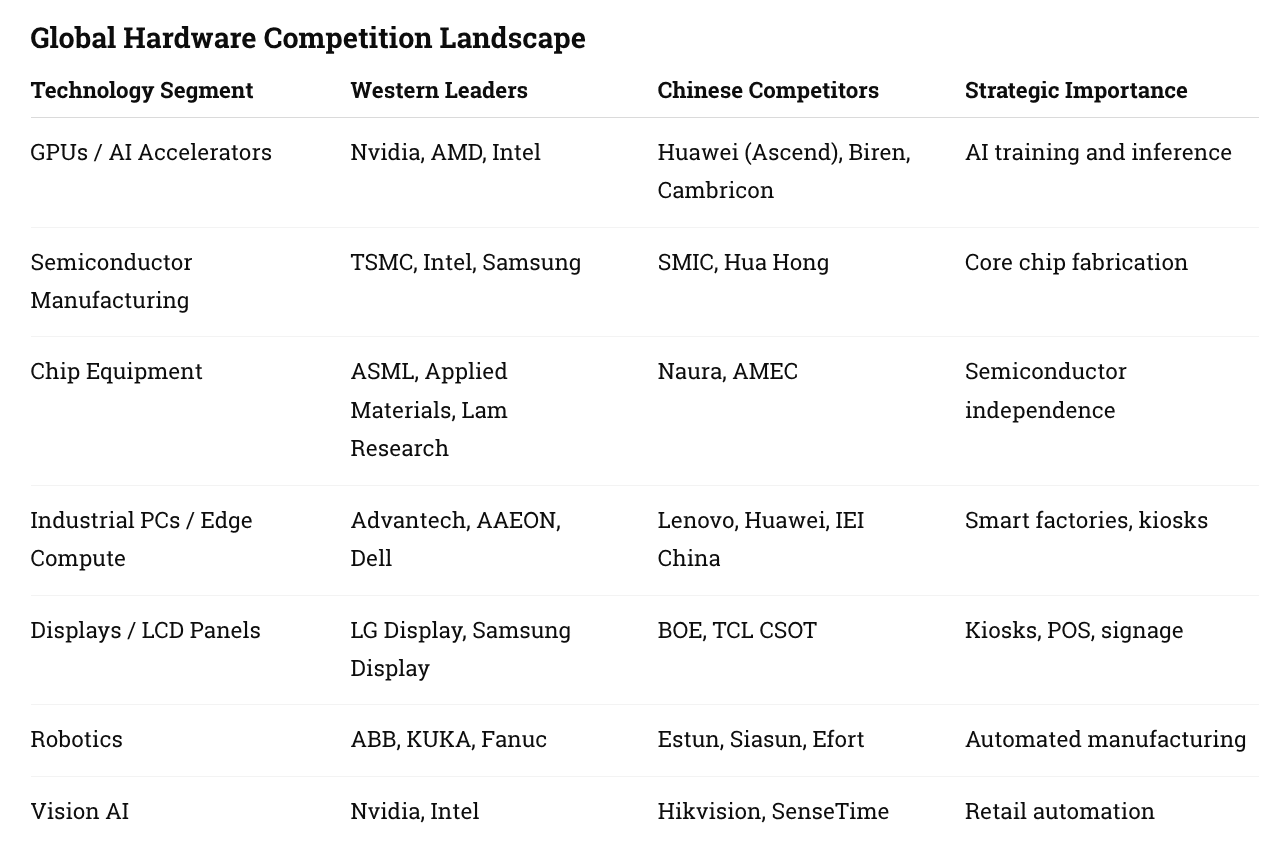

1. Global Hardware Competition Snapshot

One of the most important implications of China’s 15th Five-Year Plan is the acceleration of domestic alternatives to Western technology vendors. In several hardware sectors, Chinese firms are already becoming competitive.

One of the most important implications of China’s 15th Five-Year Plan is the acceleration of domestic alternatives to Western technology vendors. In several hardware sectors, Chinese firms are already becoming competitive.

China already dominates display panel manufacturing, which is a critical component for:

-

kiosks

-

digital signage

-

POS terminals

-

self-checkout

Companies like BOE and TCL CSOT now control more than half of global LCD production capacity, giving China a structural advantage in hardware ecosystems that depend on screens.

2. Timeline: China’s Technology Self-Reliance Strategy

China’s 15th Five-Year Plan did not emerge in isolation. It is part of a decade-long push toward technology independence.

Key Milestones

2015 – Made in China 2025

China launches its industrial policy to upgrade manufacturing and reduce reliance on foreign technology.

2019 – U.S. Technology Restrictions

Export controls on Huawei and other companies accelerate China’s push for domestic alternatives.

2020 – Dual Circulation Strategy

Beijing prioritizes domestic innovation and internal supply chains to reduce external vulnerabilities.

2021–2025 – 14th Five-Year Plan

Major investments in AI, semiconductors, and advanced manufacturing.

2026–2030 – 15th Five-Year Plan

Focus shifts to:

-

technological self-reliance

-

domestic chip ecosystems

-

AI computing infrastructure

-

robotics and industrial automation

This phase emphasizes scaling domestic technology deployment, not just research.

3. Why This Matters for Self-Service and Kiosk Hardware

For the self-service technology sector, China’s policy push could reshape the underlying hardware stack.

Three Likely Changes

1. Expansion of Chinese Edge Computing Platforms

Domestic mini-PC and embedded computing ecosystems are expected to grow rapidly, including:

-

ARM-based processors

-

AI accelerators

-

industrial edge servers

These systems could compete with platforms from Intel, AMD, and Nvidia.

2. Lower Hardware Costs

China’s manufacturing scale may reduce prices for:

-

touchscreens

-

LCD panels

-

kiosk enclosures

-

embedded motherboards

This could accelerate global deployment of self-service infrastructure.

3. Faster AI Integration in Physical Retail

Government investment in AI hardware could accelerate technologies used in kiosks and unattended retail, including:

-

computer vision checkout

-

facial recognition authentication

-

voice ordering systems

-

automated retail analytics

China is already deploying these technologies at scale in airports, hospitals, and transportation hubs.

Strategic Takeaway

China’s 15th Five-Year Plan is not simply an economic roadmap. It is a coordinated effort to build a fully domestic technology ecosystem capable of competing with Western hardware platforms.

For global technology markets, this could lead to:

-

stronger Chinese hardware competitors

-

increased supply-chain fragmentation

-

parallel technology ecosystems across geopolitical regions

Industries that rely heavily on embedded computing—including kiosks, digital signage, and unattended retail—are likely to feel these shifts first.

Global Kiosk Hardware Supply Chain Concentration

While software often dominates discussions about digital transformation, the self-service ecosystem is fundamentally hardware-driven. Kiosks, self-checkout terminals, and digital wayfinding systems rely on a layered stack of physical components sourced from multiple regions.

China already plays a major role in several of these layers.

Self-Service Hardware Supply Chain

| Hardware Layer | Primary Global Suppliers | China Market Position |

|---|---|---|

| LCD Panels / Displays | BOE, TCL CSOT, LG Display, AUO | Global leader in LCD manufacturing |

| Touchscreens | ELO, Zytronic, TPK, GIS | Strong manufacturing base |

| Embedded CPUs | Intel, AMD, ARM ecosystem | Growing domestic chip push |

| Edge AI Modules | Nvidia, Intel, Qualcomm | Huawei, Cambricon emerging |

| Industrial PCs / Mini PCs | Advantech, AAEON, ASUS | Lenovo, Huawei expanding |

| Kiosk Enclosures | Olea, Pyramid, Kiosk Information Systems | Large Chinese OEM ecosystem |

| Payment Hardware | Ingenico, Verifone, NCR | Domestic Chinese alternatives expanding |

China’s dominance in display manufacturing is particularly significant. Companies like BOE and TCL CSOT collectively account for a majority share of global LCD panel production. Because displays are often the single most expensive component in a kiosk, this manufacturing advantage gives China considerable leverage across the self-service hardware ecosystem.

As domestic semiconductor and AI chip capabilities expand under the 15th Five-Year Plan, China could gradually increase its influence across additional layers of the stack.

The Self-Service Hardware Stack

Self-service technology is often discussed as software or AI innovation, but it ultimately rests on a four-layer hardware foundation.

Understanding this stack helps explain why China’s industrial strategy matters to industries like kiosks, digital signage, and unattended retail.

Layer 1: Displays and Interfaces

User interaction begins with:

-

LCD or OLED panels

-

touch sensors

-

industrial glass

-

enclosure design

China already dominates the global supply of LCD panels used in kiosks and POS terminals.

Layer 2: Embedded Computing

This layer includes the systems that run kiosk applications:

-

industrial mini PCs

-

ARM edge processors

-

embedded motherboards

-

storage and memory modules

Western suppliers such as Intel and AMD remain dominant here, but Chinese manufacturers are expanding domestic alternatives.

Layer 3: Edge AI Processing

The next generation of kiosks increasingly incorporates AI hardware to enable:

-

computer vision

-

biometric authentication

-

fraud detection

-

automated checkout

AI accelerators from Nvidia and Intel dominate globally today, but China is investing heavily in alternatives such as Huawei Ascend processors and Cambricon AI chips.

Layer 4: Payments and Security

The final layer enables transactions and compliance:

-

EMV payment terminals

-

NFC contactless readers

-

biometric security modules

-

identity verification systems

Payment hardware remains heavily regulated and internationally integrated, but domestic Chinese providers are expanding in this space as well.

Strategic Implication for the Self-Service Industry

Taken together, these layers form the hardware backbone of the global self-service economy, which analysts estimate could represent a $150–200 billion technology ecosystem when hardware, software, and services are combined.

China’s industrial strategy aims to strengthen domestic capabilities across each of these layers.

If successful, the result may be a parallel hardware ecosystem in which:

-

Chinese platforms power domestic infrastructure

-

Western platforms dominate North America and Europe

-

emerging markets adopt a mix of both

For kiosk manufacturers, integrators, and component suppliers, this shift could reshape component sourcing, pricing, and innovation pathways over the next decade.

Resources

- How Will China’s 15th Five-Year Plan Accelerate Tech Self-Reliance in Hardware?

- How Does the $200 AI Retrofit Compare to China’s AI-Native Smart Terminals?

- StarVision Introduction

- The “Digital Divide” Paradox: When Healthcare Automation Becomes the Barrier

Designing Kiosks To Be Inclusive Efficiency vs. Empathy: A Decade of Rapid Digitization For ten years, the global healthcare mission has been …

- Acer Repositions With Posiflex Buy

Implications for Posiflex Group (Posiflex, Portwell, KIS) TAIPEI (February 21, 2025), Acer Inc. (TWSE: 2353) announced plans to acquire 25.6% of …

- Phygital 2.0: When AI Becomes Retail Infrastructure

From “Unmanned Stores” to Intelligent Retail Systems Around 2018, the global retail industry became fascinated with the idea of the “unmanned …

- Edge Computing AI and the Future of Self-Service Infrastructure

Edge Computing – Hardware and Software Across the global self-service industry, kiosks are no longer simple transaction machines. In 2026, many …

- Best POS for Small Restaurants (and ones to Avoid)

Top POS for Small Restaurants Based on the article from Kiosk Industry, here is a summary of the top-rated restaurant POS …

Subject Hubs aka Content Pillars

- Self-Service Technology Statistics

- Services — End-to-end consulting, deployment, and integration for enterprise self-service networks.

- Kiosk Hardware — Explore ADA-compliant enclosures, high-nit digital displays, outdoor, peripherals, and enterprise-ready compute engines

- Kiosk Software – Software for secure, interactive, and manageable.

- Healthcare– Modernizing the patient and staff journey. Discover the hardware and compliance standards.

- Edge AI – Eliminate cloud latency and protect data privacy by processing computer vision and natural language locally via NPU-integrated processors and M.2 module retrofits. Save energy dollars and meet PCI DSS better and automatically.

- Edge Computing

End of Content