Last Updated on July 6, 2026 by Craig Allen Keefner

Payment processors now sit at the center of how money moves in retail, restaurants, and unattended vending, with a clear shift toward integrated software, omnichannel, and contactless-first experiences.

1. Big picture: who the processors are now

-

Consolidated but crowded market. A handful of large platforms (Global Payments/Worldpay, Fiserv, FIS, Stripe, Adyen, PayPal, Block/Square, Worldline/Ingenico, etc.) handle a big chunk of global volume, but thousands of smaller processors, ISOs, gateways, and ISV-led solutions sit on top or alongside them. Payment market overview

-

Software-led payments. In all three markets (retail, restaurants, vending), the “processor” is increasingly packaged inside POS, e‑commerce, or kiosk software; many restaurant tech vendors, for example, now roll out their own “native” payment processing with bundled rates.

-

Omnichannel is the default. Processors that can handle in‑store, mobile, web, delivery, and subscription/loyalty payments on the same tokenized customer profile and reporting stack are winning RFPs at the mid‑market and enterprise tiers.

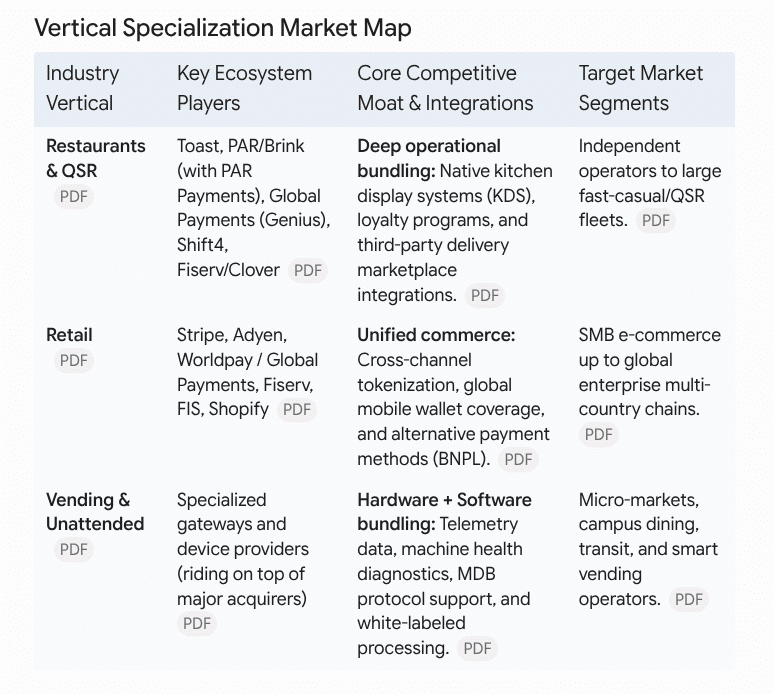

2. Restaurants and QSR: deeply integrated, mobile-first

-

Digital payments are now core. Mobile payments have overtaken cash and, in some segments, traditional cards as the primary method, with contactless (NFC wallets, tap-to-pay cards) and QR ordering becoming expected by guests.

-

Consumer preference is clear. Around half of U.S. consumers regularly use contactless methods such as tap cards and mobile wallets, and more than 50% say contactless is one of their top three priorities when choosing where to dine.

-

Embedded and bundled processing. Many restaurant tech providers (online ordering, catering, delivery integrations) now require operators to use their in‑house or preferred processor for digital orders, often at higher, less negotiable rates.

-

Operational pain points. Operators often juggle separate processors for on‑prem POS and online channels, leading to multiple merchant accounts, inconsistent rates, and complex chargeback management across platforms.

-

Processor-agnostic pushback. As margins get squeezed (typical restaurant credit card fees hover in the ~2–3% range on thin 3–5% operating margins), larger groups increasingly look for processor‑agnostic platforms that allow them to negotiate acquiring and keep digital, kiosk, and in‑store payments unified.

Illustration: A 50‑unit fast‑casual brand might run one processor embedded in its POS for dine‑in and another bundled with its delivery marketplace ordering, plus wallet payments via a third‑party gateway, all of which the finance team then has to reconcile each period.

3. Retail: omnichannel, wallets, and alternative payments

-

Unified commerce expectations. Retailers increasingly expect their processor to support online checkout, in‑store POS, mobile clienteling devices, curbside pickup, and self‑checkout from one platform, with consistent tokenization and customer identity.

-

Wallets and BNPL. In addition to debit/credit, processors must support Apple Pay, Google Pay, regional wallets, and often buy‑now‑pay‑later (Klarna, Afterpay, etc.), all with fraud controls and SCA/3DS where required.

-

Self‑checkout and self‑service. Retail self‑checkout lanes, mobile scan‑and‑go, and in‑aisle kiosks rely on semi‑integrated or fully integrated payment devices certified to specific acquirers; processors that have broad device certifications and remote management are preferred in multi‑country chains.

-

Pricing and transparency. For SMB retail, flat‑rate, bundled solutions (Square, Shopify, Lightspeed, Clover, Toast Retail, etc.) compete with interchange‑plus contracts offered by traditional processors and ISOs; the trade‑off is simplicity versus negotiability and control.

4. Vending and unattended: from cash boxes to connected commerce

-

Shift to cashless and contactless. Modern vending and micro‑markets are rapidly moving toward contactless cards and mobile wallets; in many environments (offices, campuses, transit) cash usage has collapsed, and machines that don’t accept cashless see significantly lower sales.

-

Specialized unattended processors. While the same large acquirers are typically behind the scenes, the front end often runs through specialized unattended gateways and hardware providers that support MDB, cashless readers, and telemetry for vending and micromarkets.

-

Embedded value and accounts. Closed‑loop stored value (employee wallets, campus cards, app‑based balances) is increasingly layered on top of open‑loop card acceptance, so processors need to support hybrid schemes with account management, loyalty, and offline authorization strategies for machines.

-

Remote management and fleet data. Processors and their ISV partners now sell value based on fleet telemetry (machine status, SKUs sold, route optimization) as much as on interchange; vending operators expect dashboards that marry payments, inventory, and device health.

5. Processor footprint

-

Convergence via ISVs and platforms. In restaurants and retail, the “processor footprint” is increasingly defined by which ISV platforms (POS, kiosk, e‑com, vending platforms) a given acquirer is integrated with, not just by direct merchant contracts.

Proessor and market comparison table

-

Getting deep in the weeds — Regulatory and cost pressure. Interchange caps in some regions, PCI/EMV compliance burdens, and increasingly sophisticated fraud controls (3DS, risk rule engines) shape how processors design their offerings and price them.

6. What this means for operators and vendors

-

Expect more bundling. Many POS and ordering vendors will keep tightening the bundle between software and payments, using payments margin as their business model and limiting “bring‑your‑own‑processor” options.

-

Negotiation leverage shifts to larger fleets. The more volume an operator can consolidate with one processor across retail, restaurant, and unattended, the more leverage they have on pricing and roadmap influence.

-

Technical integration is the differentiator. For kiosks, vending, and hybrid environments, processors with mature APIs, wide device certifications, and support for tokenization across channels will be better positioned than those selling just a merchant account.

Restaurants and QSR: self-service as a payments hub

In restaurants and QSR, self-service now spans:

-

Order‑ahead apps and web ordering.

-

In‑store kiosks and digital menu boards.

-

QR order-and-pay at table.

-

Drive‑thru screens and outdoor kiosks.

-

Delivery marketplaces and white‑label delivery.

Every one of those channels touches a processor, and many chains discover they’ve accumulated three or more different processing relationships without realizing it.

The Payment Processing Ecosystem: Who Does What

Payment processing involves eight key players, each with a specific role and risk. Understanding who they are and what they do is essential for troubleshooting problems and negotiating better rates.

To navigate this shifting landscape, operators must look past the consumer interface and understand the underlying technical architecture. Every transactional channel relies on a complex chain of data handoffs across eight core participants.

The Eight Participants in Every Transaction

Cardholder (Your Customer)

Initiates the transaction by providing card data (swipe, insert, tap, or online entry). The cardholder’s bank (issuing bank) verifies their identity and funds, then authorizes or declines the transaction.

Merchant (You)

Accepts the payment and submits it for processing. You’re responsible for PCI DSS compliance, accurate transaction records, and dispute resolution.

Payment Gateway

Your technical entry point. The gateway encrypts card data at your POS or checkout form and securely transmits it to the payment processor. It’s the “door” between your business and the payment system. The gateway also handles tokenization—replacing sensitive card details with a reusable token so you never store the full card number.

Payment Processor

The operational engine. It receives your transaction from the gateway, validates it, routes it through the card network to the issuing bank for authorization, and then manages clearing and settlement. The processor also handles refunds, chargebacks, and dispute resolution. Most processors also manage your merchant account and control your reserves and payout schedule.

Acquiring Bank (Your Bank)

Provides your merchant account and holds funds pending settlement. When a transaction clears, the acquiring bank receives money from the card network and deposits it into your account, minus processing fees.

Issuing Bank (Customer’s Bank)

The customer’s financial institution. During authorization, the issuing bank checks the cardholder’s available credit or funds, performs fraud checks, and either approves or declines the transaction in real time.

Card Network (Visa, Mastercard, American Express)

The infrastructure operator. Networks set rules, manage routing between issuers and acquirers, operate clearing and settlement systems, and update security standards (like 3D Secure 2). They also collect fees from merchants and issuers. Official interchange tables for 2026 are available from Visa USA Interchange Reimbursement Fees and Mastercard U.S. Region Interchange Rates.

Merchant Account

A specialized holding account where your processor deposits cleared funds before they reach your main business bank account. The merchant account is where reserves and disputes are managed.

Helpful Self-Service Payment Resources

- Ingenico Payment

- Sitekiosk Interactive Software

- Crane CPI – all types of payment

- Innovative Technology – Cash Experts

- FEC Kiosks – custom kiosks & standard kiosks

- UCP Unattended Payments – all types of payment terminals

- Datacap Systems, Inc. — kiosk payment systems and merchant account software

- NMI — NMI is a leading payment gateway and technology provider in the fintech industry.

Keywords

self service payments, self service kiosks, payment processors, retail payment processing, restaurant payment processing, vending payment solutions, unattended payments, omnichannel payments, integrated pos, kiosk payment terminals, contactless payments, nfc payments, mobile wallet payments, digital ordering, self checkout systems, quick service restaurant payments, qsr kiosks, micro market payments, smart vending machines, emv payment devices, pci compliance, payment gateways, merchant acquiring, tokenization, omnichannel commerce, unified commerce, card not present payments, card present payments, embedded payments, isv payment integrations